- Homepage

Blog - Tmob | Thinks Mobility

Blog - Tmob | Thinks Mobility - Future of Banking is Branchless: How N26 Built a Banking Empire in Europe in Less Than A Decade

Future of Banking is Branchless: How N26 Built a Banking Empire in Europe in Less Than A Decade

For more than a decade, banking as we know has been undergoing a constant transformation. Today, when we hear the word “bank,” we no longer picture a physical branch filled with workers and computers in our heads; instead, we think of a simple application. Well, especially if we’re talking about the younger generations of users, and branchless banks & FinTechs like N26, Revolut, and Monzo had seen the demand in advance and opened a new path in banking: all-digital, branchless banks.

The CFO and co-founder of N26, Maximilian Tayenthal talks about the immense change in only five years with the following:

Today, more than 10,000 customers join the N26 ecosystem in a day, and the start-up is one of the game-changers, not only in Europe but on a global scale, since the massive demand for the new-age banking model is also transforming the conventional banking approach. Teyenthal thinks players like N26 are not here to kill the brick and mortar banks, but it’s also no secret that they need to adapt quickly:

- N26 is Transforming the Everyday Finance in Europe

- N26 is not the Only Branchless Bank to Change the European Climate

- Digital Banks are Going Nowhere, and More Countries are Stepping In

- Russia’s Tinkoff is Transforming Banking in Eastern Europe

- Next Stop: Turkey

- Advantages of Digital Banking

- Join the Digital Banking Revolution with Tmob

N26 is Transforming the Everyday Finance in Europe

Founded in Germany in 2013, N26 began its quest to revolutionize everyday finance with new-age technologies that the end-user was not very used to up until those days: a branchless banking-like system that let its customers perform everyday financial tasks via a smartphone app. In less than a decade, the start-up expanded to the continent, and last year, Europe’s fastest-growing “mobile bank” began its US operations.

Of course, the first couple of years when people, especially the German population who still relied on cash or brick and mortar banks, it wasn’t all fun and games for N26. But since the pandemic, the company began breaking growth records, reaching 5 million users from 3,6 in 2019, and 7 million in January 2021. With its US launch, it’s only a matter of time that the branchless neobank will hit 10 million customers.

N26 is not the Only Branchless Bank to Change the European Climate

N26 may have launched in 2013, but the story of the new-age banking model dates as far back as 2008, to the global banking crisis and the UK’s answer to getting its most durable industry back on track. With challenger banks joining the game, the world began to see a new approach to banking. In turn, challenger banks entering the arena accelerated the development of financial technologies, which opened a window for FinTechs to emerge, and in some cases, to even become as powerful as banks. Today, when we look at the most influential banks in the Eurozone, we see FinTechs from that time that went on growing by getting digital banking licenses. N26, Revolut, Monzo, Tide, and Starling Bank are a few of the shining stars of this new way of banking, and with open-banking regulations becoming widespread globally, we’ll soon witness even more new companies joining the banking industry.

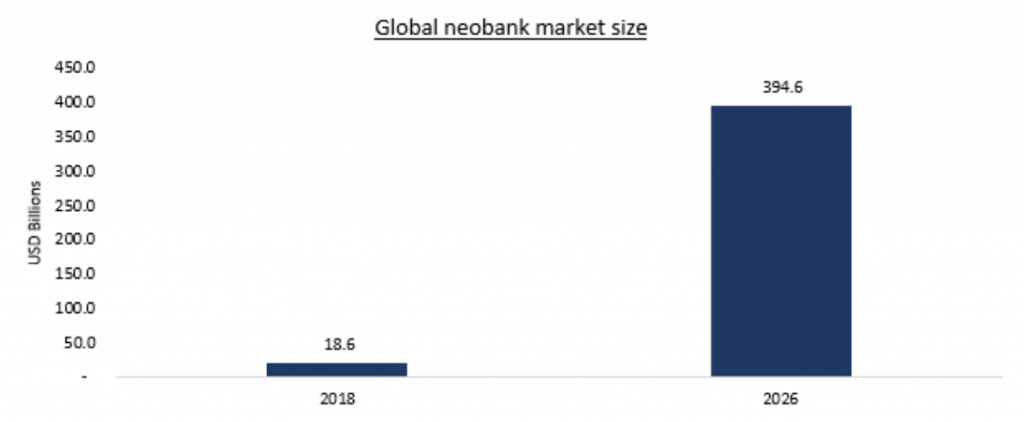

Televisory’s report on the unstoppable rise of digital banks shows us that the market is expected to rise as much as $394,6 billion in five years, but the projections belonged to the pre-vaccine pandemic era, during which FinTechs and neobanks were affected by the global slowdown of the investors.

Yes, the pandemic may have slowed down the venture capital funding for FinTechs and digital banks, but McKinsey & Company’s advisory report on the matter reveals that the industry will go back to normal sooner than almost everything else. In an atmosphere of approximately 11% economic contraction in European countries, we can safely say that digital banks are the lucky members of the financial sector.

On the other hand, Research Dive paints a much brighter picture for digital banking in general in its April 2021 research, stating that the market is anticipated to reach $ 1610 Billion by 2027, growing at a CAGR of 8.9% during the forecast period, and Revolut’s latest $800 million funding proves later, which has turned the London-based digital banking start-up into the most valuable tech company of the UK of all time.

Revolut, one of the most influential digital banking start-ups in the world, has grown its revenue by 57% in 2020.

Digital Banks are Going Nowhere, and More Countries are Stepping In

There is no doubt that FinTechs and digital banks are in constant growth. In 2019, 24 financial services start-ups hit a valuation of more than $1 billion, a considerable amount of which have already gotten their digital banking licenses.

When we say a digital bank, aka branchless bank, it’s not always the same type of financial institution that comes to mind, unlike conventional brick and mortar banks. New digital banks like Orange Bank, which had originated as a telco-offered financial service, our client Vive Bank, which takes advantage of the conveniences of open banking regulations, and most popular of all, Revolut, are three unique branchless banks models that come to mind at first thought. Especially after many countries in the European Union have made it extremely easy to apply for a digital banking license after PSD2 regulations, FinTechs and mobile financial services of once are jıining the battle of the banks, and Eastern Europe is joining the game now as well.

Russia’s Tinkoff is Transforming Banking in Eastern Europe

Seeing Europe as a whole when it comes to adopting new technologies would be too naive, and when it comes to digital banking, we see the same pattern. Yes, N26 and Revolut may be changing the picture in Western and Central Europe, but on the eastern front, we see yet another strong name from Russia: Tinkoff Bank. Founded in 2006 as a branchless credit card company, Tinkoff has been one of the major players in the digital money transformation of Russia and lately Eastern Europe.

Seeing the massive demand in the branchless bank area, Tinkoff took quick action to reinvent itself as a full-service digital bank, and in 2019, the digital bank took advantage of the latest regulations and updated its mobile banking app with the capabilities of a super-app. With the pandemic joining the picture, Tinkoff gained back what it invested in a short time. In a year, Tinkoff expanded its client base by 25% with nearly 15 million users at the end of December 2020, and the growth continues with Eastern Europe expansions.

Next Stop: Turkey

As the hub for financial technologies in Eurasia, Turkey seems to be the next player to accelerate the digital banking revolution in the area. Especially with younger generations joining the economic system, the country has seen a boom in FinTech investment and usage. According to BKM’s report, 31% of the young population (19 million) is unbanked in the country, and FinTechs are filling a huge part of the gap. Two of our clients – Vodafone Pay and Paycell, with more than 4.5 million users – have increased their investments in mobile financial services to meet the ever-rising demand for new-age financial services. Our client, Vodafone Turkey, seems very satisfied with the outcomes of Vodafone Pay, which is on the verge of expanding to six more European countries later this year with Tmob’s Mobile Financial Services Platform. Other players like Ininal which has reached 4 million users and Papara with more than 7 million users, are continuing their growth at full pace.

According to Bloomberg Turkey, the Banking Regulation and Supervision Agency of Turkey has begun working on launching new regulations that will let digital-only banks emerge.

Considering 15 million+ active non-banked FinTech users in the country, a new wave of change for branchless and digital banking in Turkey is right around the corner.

Advantages of Digital Banking

Although online and mobile banking are not new concepts in the financial sector and conventional banks have many conveniences that help solve the problems of the end-user, they differ from digital and branchless banks on many levels. Based on their own regulative set of rules, branchless banks have a wider reach, increased convenience, and advanced mobile technologies. In the end, classifying digital banks as the biggest rivals of brick and mortar banks would be fundamentally wrong, as financial institutions are one of the best examples where the old nurture new, and vice versa.

Reachability

The first advantage of the branchless or digital banking model is that it fits the zeitgeist better than the conventional models. In a world where there is a considerable amount of unbanked population that needs to integrate into the digital economy, visiting a physical bank to open an account is still a challenge, and digital banking solves this problem on day one.

Working Hours is a Thing of the Past

Thanks to their game-changing technology, digital banks have changed the way customers interact with banks in general in many countries. Only a couple of years ago, customers had to make transactions within working hours, but after the digital banking revolution and new open banking regulations that came with it, almost every bank now allows its users to perform transactions anytime they need.

Open Banking Integrations Let Super Apps Evolve

Digital banks, FinTechs, and even mobile payment apps are all going forward after open banking regulations became mainstream. In the end, they are offering more to their customers with a single application that works as a financial hub for all of their financial needs. If things go like this, we’re going to hear the super app term more and more, and it’s probably going to change the whole financial atmosphere even more dramatically than the previous decade.

Join the Digital Banking Revolution with Tmob

“Times are changing” may be one of the most popular cliche phrases of the last century, but it’s becoming more true every day! Only a couple of years ago, it was almost impossible in most European countries to gain a digital banking license. Today, many of the continent’s game-changing financial institutions are FinTechs or neobanks that used to be FinTechs. Speaking as a software company that focuses on financial technologies, we can safely say that the transformation is going to be even quicker in the future, and we are here to help.

Here at Thinks Mobility, we have been developing platforms for years. Our clients include conventional banks, branchless banks, telecommunication companies that offer mobile financial solutions, and more. In this article, we have mentioned many successful FinTech and digital banking start-ups, a majority of which outsource their technology needs to keep up with the pace of modern development. To see how you can adapt to the new age of finances with an upper hand by outsourcing technology, read our blog post.

To see what you can do with our two main FinTech & E-Banking platforms, visit our pages by clicking the links below:

Who are We?

Tmob | Thinks Mobility is a global technology powerhouse, specialized in digitalization and integration solutions, bringing growth and success to businesses and partners with its innovative SaaS, PaaS, and premium solutions since 2009 with Tmob Turkiye (TR) and Tmob United Kingdom (UK) headquarters.

Sources: 1 https://www.netguru.com/blog/n26-fintech-disruption-digital-banking 2 Dawn of the digital banking – Neobanks - Blogs - Televisory 3 A new path to profit for European fintech companies | McKinsey 4 https://www.researchdive.com/53/digital-banking-market 5 https://www.ft.com/content/4d7b739c-ffbb-4a29-ac5b-4e7dfddff5ae 6 https://techcrunch.com/2021/06/21/revolut-revenue-grew-by-57-in-2020/ 7 https://www.euromoney.com/article/28ncuyapscgma5fyuwjcw/awards/awards-for-excellence/cees-best-digital-bank-2021-tinkoff-bank 8 How will MenaPay Transform the Unbanked Population in Turkey? | by Sera Akinci | MenaPay | Medium 9 https://www.dunya.com/sirketler/paycellin-aktif-kullanici-sayisi-45-milyonu-asti-haberi-600948 10 4 milyon kullanıcısı olan ininal Kart'a temassız ve çip özelliği eklendi - egirişim (egirisim.com) 11 Ailemiz büyüdü, 7 milyonu geçti! (papara.com) 12 BDDK dijital banka lisansı vermeye başlayacak - BLOOMBERG HT (ampproject.org) 13 https://thinksmobility.com/blog-why-retail-stores-should-outsource-technology-while-adopting-the-digital-revolution/

- N26 is Transforming the Everyday Finance in Europe

- N26 is not the Only Branchless Bank to Change the European Climate

- Digital Banks are Going Nowhere, and More Countries are Stepping In

- Russia’s Tinkoff is Transforming Banking in Eastern Europe

- Next Stop: Turkey

- Advantages of Digital Banking

- Join the Digital Banking Revolution with Tmob

Related Posts

Digital Transformation of Airlines

When it comes to Digital Transformation of Airlines, Tmob providethe best digital technologies to improve the customer experience.

Financial Services: 7 Emerging Technology Trends That will Accelerate Your Digital Transformation

With emerging technology trends, FinTechs have become as reliable as banking systems without the need for procedures. Learn more!

Top Fintech Trends to Look Out for In 2023

What does the future hold for fintech? Find out with these top fintech trends connected finance apps, sustainability in finance, and more.